III. Reporting Requirements and Deadlines for Singaporean Financial Institutions

In Singapore, financial institutions (including banks, trust companies, asset management firms, insurance companies, etc.) are central to CRS and FATCA compliance. They must fulfill stringent due diligence and information reporting obligations.

SGFIs are required to identify the tax residency of their account holders and controlling persons (for entity accounts). This is typically done through Self-Certification Forms. For existing accounts, SGFIs review”non-resident indicia” (such as non-Singapore addresses, phone numbers, standing instructions, etc.) in the account information.

SGFIs must annually report the identified U.S. account holder information (FATCA) and non-Singapore tax resident account information (CRS) to IRAS.

- Reporting Deadline: May 31st annually, SGFIs must submit the previous year’s FATCA and CRS information to IRAS .

- Nil Reporting: Even if SGFIs have no reportable accounts in the reporting year, they are generally required to file a nil report to confirm their compliance status.

3. IRAS Regulation and Enforcement

IRAS strictly regulates SGFIs’ compliance with CRS and FATCA. Financial institutions failing to fulfill due diligence or information reporting obligations may face administrative penalties from IRAS, including fines. Furthermore, non-compliance can damage a financial institution’s reputation and affect its standing in the international financial system.

IV. Impact on Investors Managing Wealth in Singapore

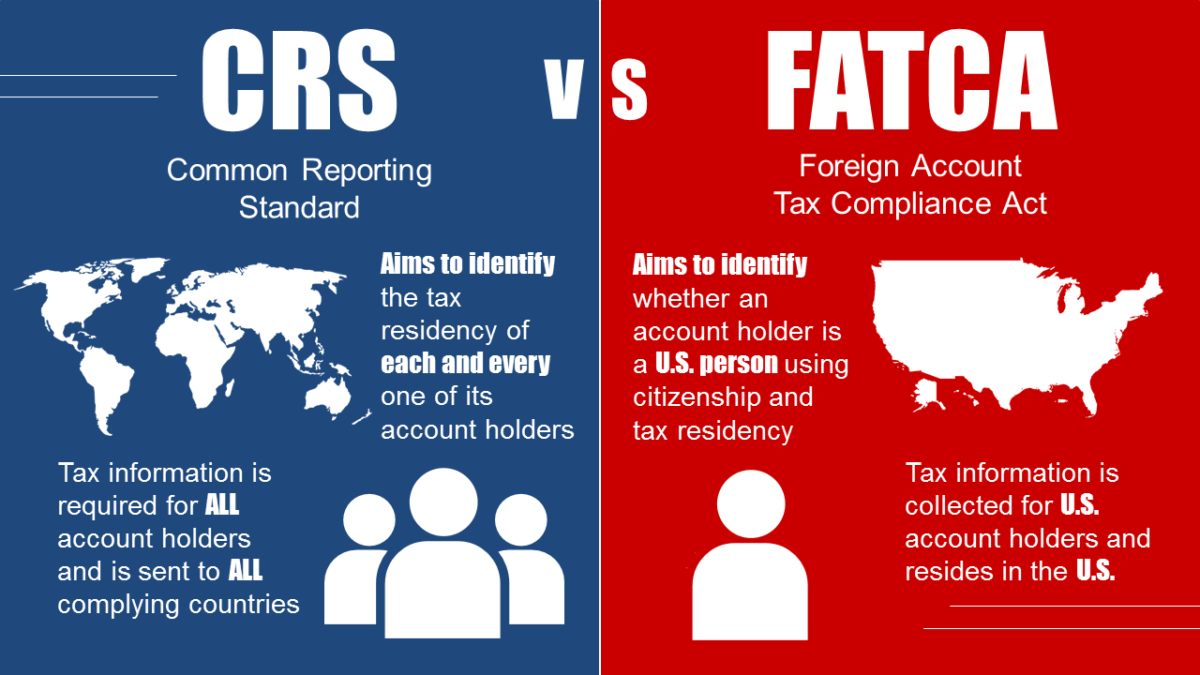

For investors choosing to manage their wealth in Singapore, particularly those from CRS participating jurisdictions like China, CRS and FATCA mean their financial assets in Singapore will no longer be “invisible.”

1. Asset Transparency: Information Exchange Between China and Singapore

Both Singapore and China are CRS participating jurisdictions and have established an information exchange relationship . This means that information on financial assets such as bank accounts, securities accounts, trusts, and funds held by Chinese tax residents in Singapore will be reported by SGFIs to IRAS, which will then exchange it with the State Taxation Administration of China. This enables Chinese tax authorities to comprehensively grasp the financial asset status of their residents in Singapore.

2. Compliance Challenges for Family Offices and Trusts

Singapore’s Family Offices and trust structures are highly favored by high-net-worth investors for their flexibility and asset protection features. However, under the CRS and FATCA frameworks, these structures must also ensure compliance.

- Entity Due Diligence: Family offices and trusts themselves may be classified as Financial Institutions or Passive Non-Financial Entities (Passive NFEs), requiring due diligence and identification of the tax residency of their controlling persons.

- Information Reporting Obligations: If a family office or trust is deemed a Reporting Financial Institution, it must fulfill CRS and FATCA reporting obligations.

Investors who fail to fully understand or timely adjust their wealth structures may face the following risks:

- Undeclared Offshore Income Risk: Chinese tax residents are subject to taxation on their global income. If income from financial assets in Singapore is not declared in China, they may face back taxes, late payment surcharges, and penalties.

- Tax Residency Disputes: Complex living arrangements can lead to ambiguous tax residency determinations, triggering multi-jurisdictional tax disputes.

V. The Professional Value of a Singapore Firm: Your Partner in Compliance and Growth

In the face of an increasingly complex international tax environment, an experienced professional firm well-versed in Singaporean and international regulations is an indispensable partner. Our services include:

1. Tax Residency Planning and Confirmation

Assisting investors in accurately determining their tax residency to avoid compliance risks arising from incorrect identification.

2. Wealth Structure Compliance Review and Optimization

Conducting CRS/FATCA compliance reviews on investors’ existing family offices, trusts, companies, and other wealth structures, and providing optimization recommendations to ensure their robust operation in the era of transparency.

3. Due Diligence and Information Reporting Assistance

Providing professional consulting and support to Singaporean financial institutions in designing CRS/FATCA due diligence processes, building systems, and reporting information to ensure they meet IRAS regulatory requirements.

4. Offshore Income Declaration and Tax Consulting

Assisting investors in understanding their tax obligations regarding offshore income, providing tax declaration consulting for China and other countries (regions), and assisting in handling inquiries from tax authorities.

5. Emerging Regulations Response: Forward-Looking Services for CARF and Immovable Property Information Exchange

Closely monitoring emerging international tax regulations such as the Crypto-Asset Reporting Framework (CARF) and the Immovable Property Information Exchange Framework (IPI Framework), and proactively planning response strategies for investors to ensure their compliance in the crypto-asset and real estate sectors.

VI. Forward-Looking Dynamics: The New Frontier of Global Tax Transparency—CARF and Immovable Property Information Exchange (CRS 2.0)

The process of global tax transparency has not halted. Beyond CRS and FATCA, the international community continues to introduce new information exchange standards to address challenges posed by emerging financial products and cross-border transactions.

1. Crypto-Asset Reporting Framework (CARF): Transparency of Digital Wealth

The Crypto-Asset Reporting Framework (CARF) is one such initiative. Spearheaded by the OECD, CARF aims to establish an international information exchange standard for crypto-asset transactions, expected to be implemented starting in 2027 . This means that the cryptocurrencies you hold, such as Bitcoin and Ethereum, as well as transactions conducted through them, will also fall under the regulatory purview of global tax authorities in the future. For investors, understanding CARF in advance and planning compliance pathways is now imperative.

2. Immovable Property Information Exchange Framework (CRS 2.0): Overseas Real Estate Enters the “Transparent Era”

Following financial accounts and crypto-assets, immovable property is also set to face stricter tax transparency regulations. The OECD is actively promoting the Framework for the Automatic Exchange of Readily Available Information on Immovable Property for Tax Purposes (IPI Framework), often referred to as “CRS 2.0” or the “Real Estate Version of CRS” .

The core of this framework lies in establishing an automatic exchange mechanism among national tax authorities for key information such as immovable property ownership, assessed value, and rental income. This means that in the future, information on global real estate held either directly in an individual’s name or indirectly through complex structures like companies, trusts, or funds will gradually be brought under the strict regulatory scope of automatic exchange.

For investors allocating real estate assets in Singapore or utilizing Singaporean entities to hold global immovable property, this is undoubtedly a policy shift with profound implications. As a hub for international real estate investment, Singapore’s financial ecosystem and professional service system are closely monitoring this trend, aiming to guide the public in reviewing the tax compliance of their immovable property holding structures, ensuring the stability and security of assets in the era of transparency.

3. Upgraded Compliance Recommendations: A Comprehensive Review of Wealth Structures

In light of these new regulations, compliance recommendations for investors must also be upgraded: it is no longer sufficient to focus solely on financial accounts and crypto-assets; a comprehensive review of immovable property holding structures must begin to ensure their tax compliance. Professional tax planning will become increasingly vital to avoid potential future tax risks and unnecessary complications.

The implementation of CRS and FATCA, along with the continuous emergence of new regulations like CARF and the IPI Framework, signifies that global tax transparency has become an irreversible trend. For investors managing wealth in Singapore, this presents both a challenge and an opportunity to achieve sustainable wealth growth through professional planning. As your trusted partner, we are dedicated to providing forward-looking, customized solutions to help you navigate changes, ensure compliance, and ultimately achieve the steady inheritance and appreciation of your wealth in a complex international tax environment.

References

- IRAS. [Foreign Account Tax Compliance Act (FATCA)](https://www.iras.gov.sg/taxes/international-tax-relations/foreign-account-tax-compliance-act-(fatca )). (Accessed April 6, 2026).

- IRAS. [Common Reporting Standard (CRS)](https://www.iras.gov.sg/taxes/international-tax-relations/common-reporting-standard-(crs )). (Accessed April 6, 2026).

- IRAS. [AEOI Reporting for Financial Institutions](https://www.iras.gov.sg/taxes/international-tax-relations/aeoi-reporting-for-financial-institutions ). (Accessed April 6, 2026).

- OECD. [CRS: Activated Exchange Relationships](https://www.oecd.org/tax/automatic-exchange/crs-by-jurisdiction/CRS-activated-exchange-relationships.pdf ). (Accessed April 6, 2026).

- OECD. [Crypto-Asset Reporting Framework (CARF)](https://www.oecd.org/tax/automatic-exchange/crypto-asset-reporting-framework/ ). (Accessed April 6, 2026).

- OECD. [Framework for the Automatic Exchange of Readily Available Information on Immovable Property for Tax Purposes](https://www.oecd.org/tax/automatic-exchange/immovable-property-information-exchange/ ). (Accessed April 6, 2026).